Relocation Payments Are Becoming an Exit Tax on Bay Area Landlords

What started as tenant assistance has become a burdensome cost of doing business—and a growing legal risk.

At first, relocation payments were sold as a simple idea: "Help tenants cover moving costs if they are evicted because of no fault of their own." Seems reasonable to give outgoing tenants a hand up with a small amount of money to make the transition, especially given the upside potential of a vacant property, right? But that's not what they are anymore. At some point in our legal careers, it changed.

In the Bay Area and in tenant-friendly cities throughout California, the relocation payments attendant to no-fault evictions have quietly transformed into something else entirely —up to a five-figure check that owners are required to write for exercising basic property rights.

In the not-too-distant past, we recall Ballinger v. The City of Oakland. When duty called for a military couple living in Oakland, they were temporarily stationed in Maryland with two children in tow. The couple kept their house and, before making the cross-country trip, leased it out on a month-to-month basis to realise rental income while they served their country.

When they were getting ready to return, a 60-day notice to vacate was served on their tenants, who happened to be tech workers with healthy salaries. Under Oakland's Uniform Residential Tenant Relocation Ordinance, however, the Ballingers were forced to pay nearly $7,000 to their well-to-do tenants before they could move back into their own home. The city declined to refund the money, and a lawsuit ensued, challenging the requirement under Oakland's relocation ordinance that landlords distribute payments when they endeavor to retake occupancy of their homes upon the expiration of the lease.

The broadsided couple claimed that the fee constitutes an unconstitutional exaction of their Oakland home, and an unconstitutional seizure of their money under the Fourth and Fourteenth Amendments. Ultimately, the ordinance survived the legal dustup.

The Numbers Are No Longer Reasonable

Let’s stop pretending these are modest payments. Relocation payments have hit record highs in 2026, and that should come as no surprise because, since they are adjusted for inflation, there is only one trajectory, and that is up. Yet most people don’t realize how big these numbers have gotten.

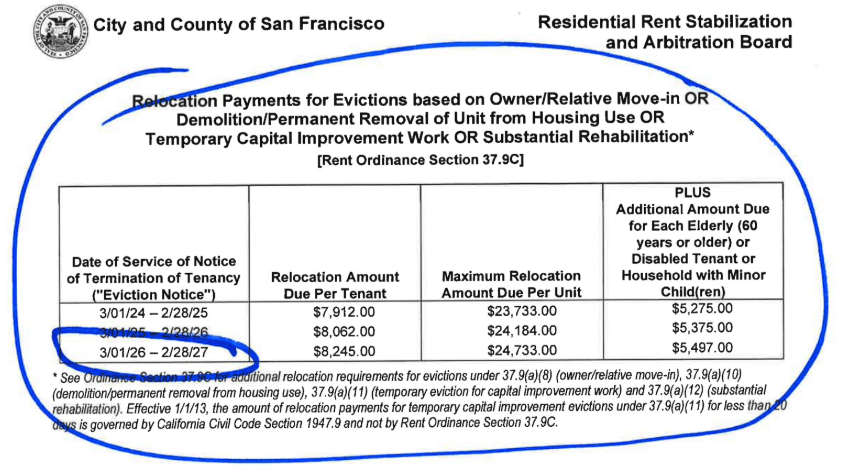

Under San Francisco’s high ceiling, per-tenant model, a landlord can expect to pay around $10K-$20K to a smaller household. In comparison, larger and protected households can easily trigger relocation payments of $20K–$25K or more. That is according to an exhibit comparing permanent relocation payments in the Bay Area. In Oakland, meanwhile, relocation payments are based on a flat per-unit model, and most cases will set landlords back around $7K–$13K. Berkeley ranks as among the highest, with most cases landing aound $20–$25K.

And keep in mind that relocation traps are not just limited to evictions anymore. Traditionally, relocation payments were synonymous with tenants being permanently displaced, but have expanded into temporary transitions necessary for repairs and code compliance, along with renovations requiring permits.

Think about this requirement to cough up a large amount of funds.

Permissible rent increases in rent-controlled jurisdictions are capped on some formula tied to inflation (San Francisco's is 1.6% effective from March 1, 2026, through February 28, 2027), effectively limiting the upside potential of the investment property. That's deflating enough.

Yet unlike rent caps that limit how much rent can be raised later on, relocation payments to outgoing tenants create a hard, immediate cash obligation to housing providers and disproportionately harm small-scale "mom and pop" landlords that often lack the liquidity to pay such astronomical checks. It doesn't matter whether or not the deal makes economic sense or not - the check still has to be cut.

Housing providers are already squeezed due to rising compliance costs, recent appliance mandates, fee restrictions, and increased legal exposure, forcing many to throw in the towel. Adding insult to injury, landlords must find a large sum of cash to move back into their own property or leave the rental business, and sadly, these cost-prohibitive payments are the final nail in the coffin for many. Parting with several thousand dollars is not "relocation assistance" in our book. It is a burden that makes it difficult, if not impossible, for owners to use their own property.